India’s Transfer Pricing documentation in accordance to BEPS’s three tier structure

Economy

347 week ago — 5 min read

Summary: Transfer Pricing is an increasingly prevalent phenomenon as globalisation brings the world, and its economies together. If your firm is one impacted by Transfer Pricing norms, here is the documentation you need to be compliant with all the laws and regulations pertaining to your business.

The Organisation of Economic Cooperation and Development (OECD) has devised a framework for countries to implement, constituting of 15 action plans as measures against BEPS. It is called the G20 BEPS Project and was endorsed by G20 Finance Ministers and Central Bank Governors in 2016.

India being a major endorser of BEPS Project has incorporated BEPS Action Plan 13 in its Finance Act 2016. BEPS Action Plan 13 elucidates a three-tier structure of TP documentation: (1) Master File (2) Country by country reporting, and (3) Local documentation file, with respect to the transactions entered into with an International Group’s (IG) overseas Associated Enterprises (AEs) or constituent entities. The TP documentation requirement is inserted as rule 10D of the Income Tax Rules, 1962 of India.

TP documentation provides the tax authorities with the required information to conduct a transfer pricing risk assessment and transfer pricing audit of an IG.

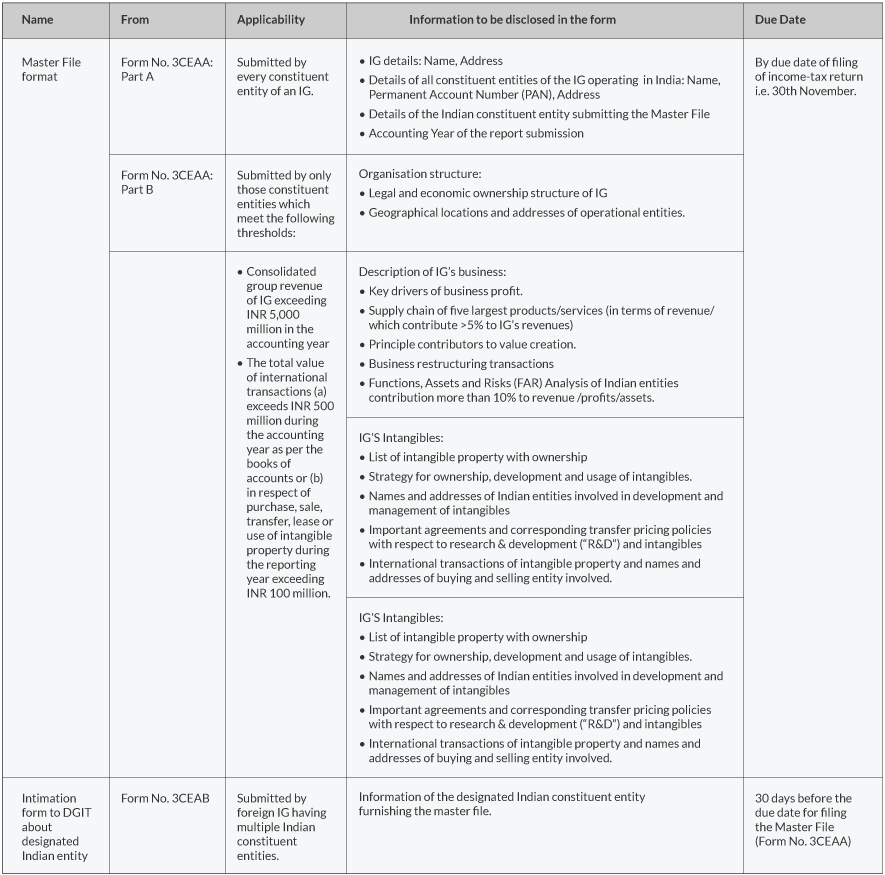

Master File

The Master File is the overall blueprint of the International Group’s (IG) global business model, constituting all operations and intercompany transfer pricing policies.

According to the Indian transfer pricing law, the following documents are to be submitted by the IG or its Indian constituency:

-

Form No. 3CEAA: Specified format of master file. The form is divided into two sections:

-

Part A of Form No. 3CEAA: It comprises of the general information about the IG and its Indian constituencies.

-

Part B of Form No. 3CEAA: It comprises of the details of the IG’s business model.

- Form No. 3CEAB: Notification of submission of master file by a particular Indian constituent entity in case of presence of multiple Indian entities of the foreign IG. The master file can be submitted by only one designated entity to Director General of Income-tax.

* The Master File in Form No. 3CEAA and the intimation in Form No. 3CEAB is to be signed by the person competent to verify the return of income of the constituent entity.

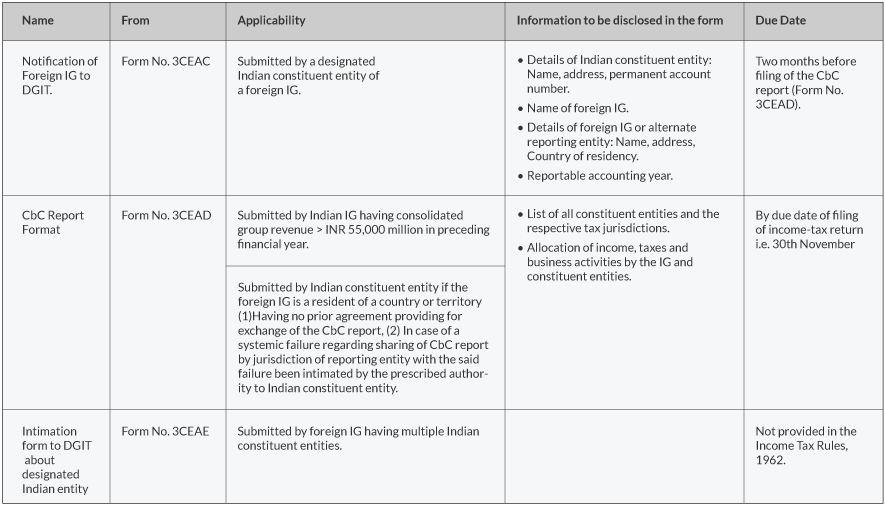

2. Country by Country (CbC) Reporting

CbC reports provide the key elements of financial statements of an IG by jurisdiction. The CbC report is used to check the authenticity of the Master file provided. Discrepancies in the information provided alerts the tax authorities to examine the IG’s structure again.

Documents to be submitted related to CbC reporting are as follows:

-

Form No. 3CEAD: Template in which information of the CbC report is to be provided.

-

Form No. 3CEAC: CbC report notification to be filed by Indian constituent entity of a foreign IG, providing the details of the foreign IG or the alternate reporting authority.

-

Form No. 3CEAE: Notification of designated Indian constituent entity which will furnish the CbC report of the IG in case of multiple Indian constituent entities. The form is to be submitted to Director General of Income-Tax.

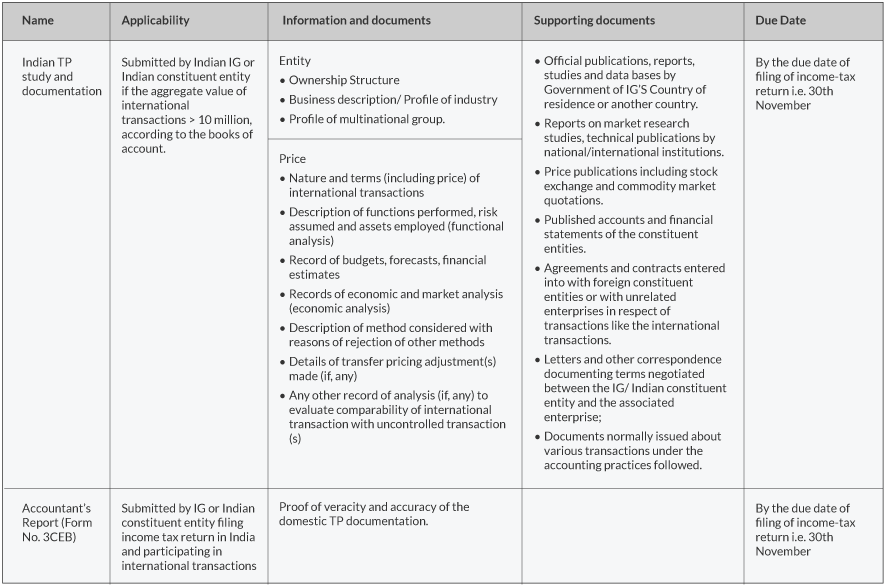

3. Local File

The local file provides information about the local company’s transactions with related parties. As the information is very similar to the information and documents required in domestic transfer pricing documentation, no changes or additions are made in Indian Transfer Pricing law.

The information and documents to be submitted for domestic TP documentation are as follows:

The TP documentation required under Income Tax Rules, 1962 is to be furnished annually. Failure to maintain or produce said documents can lead to a penalty of up to 2% of the value of each transaction, where non-compliance exists. Failure to furnish Form No. 3CEB can lead to a penalty of INR 1,00,000. Hence, organisations should adhere to timelines and maintain updated records with contemporaneous information.

To explore business opportunities, link with us by clicking on the 'Invite' button on our eBiz Card.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views, official policy or position of GlobalLinker.

Posted by

Dezan Shira and AssociatesDezan Shira & Associates is a pan-Asia, multi-disciplinary professional services firm, providing legal, tax and operational advisory to international corporate investors....

View Dezan Shira 's profile

Other articles written by Dezan Shira and Associates

Transfer Pricing: Dilemma of intangibles

354 week ago

Most read this week

Comments

Share this content

Please login or Register to join the discussion